Get Answers

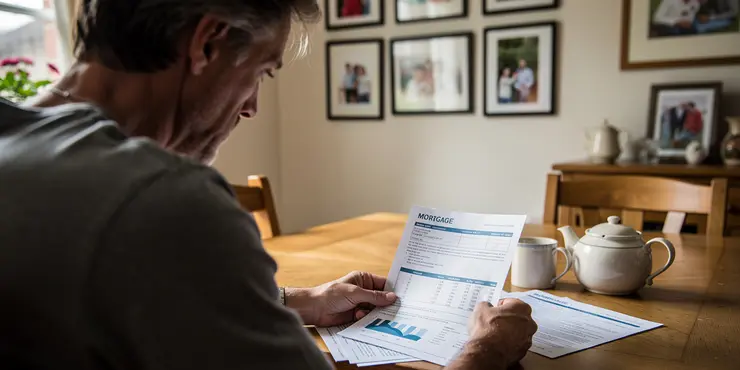

Understanding Fixed-Rate Mortgages

A fixed-rate mortgage is a type of home loan where the interest rate remains constant throughout the agreed term. In the UK, typical fixed-rate periods can range from two to ten years. This stability means that your monthly payments remain the same, providing predictability and making budgeting easier for homeowners. These mortgages are popular among individuals who prefer knowing exactly what their financial obligations will be each month.

Interest Rate Fluctuations

Interest rates can fluctuate due to various economic factors, including changes by the Bank of England to the base rate. Typically, when the base rate changes, it affects variable-rate mortgages directly. However, with a fixed-rate mortgage, you are insulated from these fluctuations during the fixed period. This means that even if the Bank of England raises or lowers the base rate, your mortgage payments during the fixed term will remain the same. This protection is one of the primary benefits of choosing a fixed-rate mortgage.

What Happens at the End of the Fixed Term?

At the end of the fixed-rate period, your mortgage usually reverts to the lender's standard variable rate (SVR). The SVR can fluctuate in line with changes to the base rate, meaning your mortgage payments could increase or decrease. As a borrower, you can choose to remortgage to a new fixed-rate deal or another type of mortgage to better suit your financial situation and objectives. Many homeowners start exploring their options months before the end of the fixed term to avoid being moved to the potentially more expensive SVR.

Taking Action During the Fixed Term

During the fixed-rate period, it is crucial to remember that breaking your agreement, such as by remortgaging early or repaying the mortgage in full, might result in penalties known as early repayment charges. These charges can be significant and are designed to compensate the lender for the interest income they expected to earn. Therefore, while your payments are fixed, any desire to change your mortgage arrangement before the term ends should be carefully considered.

Conclusion

In the UK, a fixed-rate mortgage offers protection against interest rate fluctuations, ensuring that your payments remain consistent during the agreed term. This stability provides peace of mind and assists in managing household budgets. It is, however, important to keep in mind the implications of the mortgage reverting to a variable rate at the end of the term and plan accordingly. Staying informed about potential changes and exploring new mortgage deals in advance can help maintain financial stability and optimize your home loan strategy.

Understanding Fixed-Rate Mortgages

A fixed-rate mortgage is a type of loan for buying a home. With this loan, the amount of interest you pay stays the same for a set time. In the UK, this could be from two to ten years. This means your monthly payments won't change, which makes it easier to plan your spending. Many people like this kind of loan because they know exactly how much they need to pay each month.

Interest Rate Changes

Interest rates can go up or down because of different things in the economy. The Bank of England may change the main interest rate, called the base rate. When this happens, it can affect loans where the interest rate can change. But with a fixed-rate mortgage, your payments stay the same during the fixed period, no matter what happens to the base rate. This is a big advantage of having a fixed-rate mortgage.

What Happens at the End of the Fixed Period?

When the fixed-rate time ends, your loan usually switches to something called the standard variable rate (SVR). The SVR can go up or down, which means your payments might change. Before this happens, you can choose to look for another fixed-rate deal or a different kind of loan. It’s a good idea for homeowners to start looking at their choices a few months before the fixed period ends so they aren’t surprised by changes in payments.

Making Changes During the Fixed Period

If you want to change your loan during the fixed time, like paying it off early or switching to another deal, you might have to pay fees called early repayment charges. These fees can be a lot of money because the lender was expecting to get paid the interest over the full term. So, even though your payments are stable, it’s important to think carefully before making changes to the loan before the time is up.

Conclusion

In the UK, a fixed-rate mortgage helps keep your payments the same, giving you peace of mind and making it easier to manage your money. However, remember that after the fixed period ends, your loan might change to a rate that can vary. Stay informed about any changes, and look into new mortgage deals ahead of time to keep your payments stable and make the most of your loan.

Frequently Asked Questions

A fixed-rate mortgage is a type of home loan where the interest rate remains constant throughout the duration of the loan, which means your monthly payments stay the same.

No, if you have a fixed-rate mortgage, your payments will not change if interest rates rise.

No, with a fixed-rate mortgage, the rate and payment amounts remain the same even if interest rates fall.

Fixed-rate mortgages commonly have terms of 15, 20, or 30 years.

Yes, a fixed-rate mortgage provides predictability and stability with consistent monthly payments, making budgeting easier.

No, the lender cannot change the interest rate on a fixed-rate mortgage once it is set at the start of the loan.

While property taxes may increase, affecting your escrow payments, the principal and interest portion of your fixed-rate mortgage will remain unchanged.

Yes, fixed-rate mortgages are often recommended for first-time homebuyers due to their stability and predictability.

A potential downside is that fixed-rate mortgages do not benefit from decreases in market interest rates.

If you refinance, you will replace your existing mortgage with a new one, potentially with different terms or a different type of interest rate.

Yes, you can switch from a fixed-rate to an adjustable-rate mortgage through refinancing.

Some fixed-rate mortgages may have prepayment penalties, so it’s important to check the terms of your loan agreement.

Inflation does not directly affect the terms of a fixed-rate mortgage, but it can impact your purchasing power and cost of living.

While missing a payment won’t change the set interest rate, it can lead to penalties or additional fees, affecting your overall payments.

Yes, a better credit score can secure a lower interest rate at the time of taking out the fixed-rate mortgage.

Yes, making extra payments can reduce the principal balance quicker and shorten the term of your loan.

Fixed-rate loans generally have higher initial rates than adjustable-rate loans, but they offer greater security against future increases.

Renegotiation typically requires refinancing, which involves replacing your existing mortgage with a new loan.

Consider if you value payment stability, if you plan to stay in your home for a long time, and your tolerance for interest rate fluctuations.

The process generally involves getting pre-approved, selecting a lender, completing an application, and undergoing the underwriting process before closing.

A fixed-rate mortgage is a kind of home loan. The interest rate does not change during the loan. This means your monthly payments will always be the same.

No, your payments will not change if you have a fixed-rate mortgage, even if interest rates go up.

No, if you have a fixed-rate mortgage, the amount you pay stays the same. This is true even if interest rates go down.

Fixed-rate mortgages are loans for buying a house. You can pay them back in 15, 20, or 30 years.

Yes, a fixed-rate mortgage is a loan where the amount you pay every month stays the same. This helps you plan your money better.

No, the bank cannot change the interest rate on a fixed-rate mortgage once it is set at the start of the loan.

If property taxes go up, you might pay more into escrow. But the main loan amount and the interest on your fixed-rate mortgage will not change.

Yes, fixed-rate home loans are good for people buying a house for the first time. They are steady and don't change. This makes them easier to plan for.

A fixed-rate mortgage is a type of loan where the interest rate stays the same. One downside is that if interest rates go down, your rate will not change. This means you won't pay less.

If you refinance, you get a new loan to pay off your old one on your house. This new loan might have different rules or a new kind of interest rate.

Yes, you can change your mortgage from a fixed-rate to an adjustable-rate by refinancing.

Some home loans have rules that make you pay extra money if you pay them off early. It's a good idea to read your loan papers carefully to see if this applies to you.

Inflation does not change a fixed-rate mortgage, but it can make things more expensive and affect how much you can buy with your money.

If you miss a payment, your interest rate will stay the same. But you might have to pay extra fees or penalties. This means you could end up paying more money overall.

Yes, having a good credit score can help you get a lower interest rate when you borrow money with a fixed-rate mortgage.

Yes, paying extra money can help you pay off your loan faster and make it shorter.

Fixed-rate loans usually start with higher costs than loans with changing rates. But they are safer because the costs won't go up in the future.

Changing your home loan usually means getting a new loan to replace your old one.

Think about these things:

- Do you like having the same payments every time?

- Are you planning to live in your house for a long time?

- Are you okay if interest rates go up and down?

To help you decide, you can use tools like a calculator to see how your payments might change. Talking to a financial advisor or using online resources can also give you more information.

Here is how it works:

1. First, you get pre-approval. This means the bank looks at your money and says, “Yes, you can borrow!”

2. Next, you pick a lender. A lender is a bank or company that gives you money.

3. Then, you fill out an application form. This is like answering questions about your money and what you want to borrow.

4. After that, there is an underwriting process. This is when the bank checks everything again to make sure it all makes sense.

5. Finally, you reach closing. This is when you get the money!

For help, try these tips:

- Use a friend or family member to help read the forms with you.

- Use a calculator to help with numbers.

- Ask lots of questions until you understand everything.

Ergsy Search Results

This website offers general information and is not a substitute for professional advice.

Always seek guidance from qualified professionals.

If you have any medical concerns or need urgent help, contact a healthcare professional or emergency services immediately.

Some of this content was generated with AI assistance. We've done our best to keep it accurate, helpful, and human-friendly.

- Ergsy carefully checks the information in the videos we provide here.

- Videos shown by Youtube after a video has completed, have NOT been reviewed by ERGSY.

- To view, click the arrow in centre of video.

- Most of the videos you find here will have subtitles and/or closed captions available.

- You may need to turn these on, and choose your preferred language.

- Go to the video you'd like to watch.

- If closed captions (CC) are available, settings will be visible on the bottom right of the video player.

- To turn on Captions, click settings.

- To turn off Captions, click settings again.