Get Answers

Understanding Car Finance Mis-selling

Car finance mis-selling occurs when a financial product related to car purchases is sold under misleading terms or without proper information being provided to the consumer. This can include not being informed of important features, terms, or hidden costs associated with the finance agreement.

Common Signs of Mis-sold Car Finance

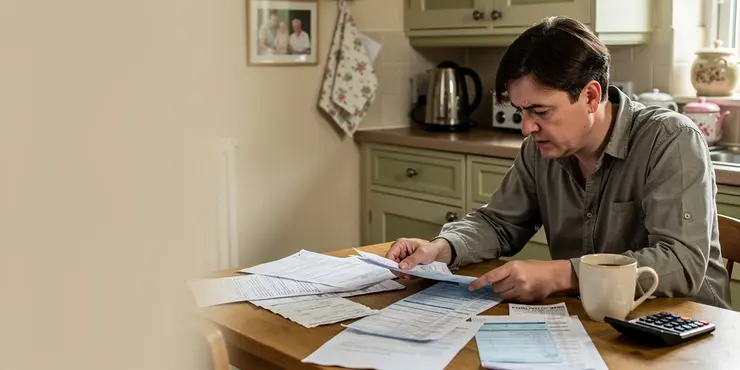

If you suspect that you have been mis-sold car finance, there are certain signs to look out for. First, check if you were informed about the full terms of the agreement, including interest rates, total repayment amounts, and any fees associated with early repayment. Sometimes, salespeople may fail to disclose important information or may apply unnecessary pressure to encourage you to sign up. If you felt rushed during the process or if certain aspects of the agreement were not clear, it may be a sign of mis-selling.

Another key indicator is whether you were given all the options available. Dealers are supposed to recommend the most suitable product for your needs, but in some cases, they may only present options that serve their financial interests, such as products with higher commissions for them.

Steps to Determine if You Were Mis-sold

To find out if you were mis-sold car finance, start by gathering all related documents, including your finance agreement, any communications from the dealer or lender, and any marketing materials you were provided with. Review these documents to ensure the terms you were verbally quoted match the written agreement. Pay special attention to interest rates, fees, and the duration of the contract.

If you spot inconsistencies or were not informed about key aspects, reach out to the dealer or lender with your questions. Ask for clarification on anything that was not explained adequately at the time of purchase. If their responses do not satisfy you, consider escalating your concerns.

Seeking Professional Advice

Consider consulting with a financial advisor or a legal expert specializing in consumer rights and finance. They can provide guidance based on the specifics of your situation and help you understand your options. It's also possible to contact organizations such as the Citizens Advice Bureau or the Financial Ombudsman Service, which can offer free advice and potentially assist with making a complaint.

Filing a Complaint

If you believe you have a strong case, you can file a formal complaint with the finance provider, outlining your concerns and any evidence you have collected. They are required to investigate your complaint and provide a response. If you remain unsatisfied, you can escalate the matter to the Financial Ombudsman Service, who will conduct an independent review.

Conclusion

Identifying mis-sold car finance requires careful review and understanding of your finance agreement. By gathering evidence, seeking advice, and following the appropriate complaint processes, you can address any mis-selling issues and seek fair resolution.

Understanding Car Finance Mis-selling

Car finance mis-selling happens when you are given car finance in a way that is not fair. This might be because important information is missing or not clear. For example, the terms, features, or costs might not be explained properly.

Common Signs of Mis-sold Car Finance

There are signs that can help you know if your car finance was mis-sold. Check if you understood all the parts of the agreement. This means knowing about interest rates, total repayments, and any fees if you repay early. Sometimes, salespeople might rush you or not tell you everything you need to know. If you felt hurried or confused, it might mean mis-selling happened.

Another sign is if you didn’t get every option available. Dealers should offer the best products for you, but sometimes they might only suggest options that benefit them financially.

Steps to Determine if You Were Mis-sold

To find out if you were mis-sold car finance, start by looking at all your documents. This includes the finance agreement and any communication from the dealer or lender. Check to see if the terms match what you were told. Look closely at interest rates, fees, and the length of the contract.

If there are differences or missing details, ask the dealer or lender for explanations. If the answers don’t satisfy you, consider taking further steps.

Seeking Professional Advice

Think about asking a financial or legal expert for help. They know about consumer rights and can advise you. Organizations like the Citizens Advice Bureau and the Financial Ombudsman Service can give free help and advice too.

Filing a Complaint

If you think you were mis-sold, make a formal complaint to the finance provider. Explain your problem and show any evidence you have. They must investigate and reply to you. If you’re still not happy, you can contact the Financial Ombudsman Service for an independent review.

Conclusion

To find out if your car finance was mis-sold, carefully check your finance agreement. Gather proof, get advice, and use the complaint process to sort out any problems.

Frequently Asked Questions

Being mis-sold car finance means you were not given the correct information or were influenced into a financial agreement that wasn't suitable for you.

Common signs include not receiving full information about the agreement, being placed on a more expensive finance product without reason, or being pressured into signing.

Review the terms and conditions of your finance agreement and compare it with what was explained to you at the time of purchase.

You can contact the Financial Ombudsman Service or a legal professional specializing in financial mis-selling.

Yes, you can file a complaint with the financial institution or dealership involved, and escalate it to the Financial Ombudsman if necessary.

You'll need the car finance agreement, any correspondence with the seller, and marketing materials or advertisements you received.

Typically, you have up to six years from the sale date, or three years from when you became aware of the issue, to make a complaint.

If your complaint is successful, you may be entitled to compensation, including a refund of fees or interest paid.

If rejected, you can appeal the decision or take your complaint to the Financial Ombudsman Service for further review.

Yes, if a finance broker provided misleading or incorrect information or guidance, they could be held responsible.

Yes, there are legal experts and claims management companies that specialize in handling mis-sold car finance cases.

Collect all relevant documents, written communication, and any records of phone calls discussing the finance terms.

If the finance terms were not suitable and you missed payments, it might have impacted your credit score.

Check for terms about interest rates, fees, early repayment charges, and compare them with what was explained during the sale.

The time can vary, but complaints typically take a few months to process, depending on the complexity and responsiveness of the parties involved.

The FCA regulates financial markets and ensures firms adhere to standards, protecting consumers from mis-selling practices.

Understanding the terms ensures you are fully aware of the financial commitments and prevents being locked into unsuitable agreements.

Online research can provide guidance, but it's advisable to seek professional advice for a thorough assessment.

Any car finance product can be mis-sold, especially if providers do not follow proper procedures and transparency practices.

Yes, you can attempt to resolve the issue directly with the dealer before involving regulatory bodies or legal proceedings.

If you were mis-sold car finance, it means someone did not give you the right information or persuaded you to agree to a money deal that was not good for you.

Here’s a tip to help: - **Ask Questions**: Always ask questions if you don't understand something. - **Use Tools**: There are apps and tools that can read text aloud or help explain difficult words. - **Take Your Time**: Don't feel rushed to make a decision. If you feel confused or unsure, it’s okay to ask a friend or family member you trust to help you.Common signs include not getting all the information about the agreement, being put on a more expensive finance plan without a reason, or being pushed into signing.

Look at the rules and promises of your money agreement. Check if it matches what was told to you when you bought it.

You can talk to the Financial Ombudsman Service. They help people with money problems. You can also talk to a lawyer who knows about money mistakes.

Yes, you can tell the bank or car dealer if you are unhappy. If they don't help, you can ask someone called the Financial Ombudsman to help you.

You will need to get some things:

- The papers about car money.

- Any letters or emails from the person who sold you the car.

- Any ads or flyers you got about the car.

You can use a helper tool like a checklist to keep everything in order.

You usually have up to 6 years from when you sold something, or 3 years from when you found out there was a problem, to say something about it.

If you win your complaint, you might get money back. This could be money you paid in fees or interest.

If they say "no," you can ask them to think about it again. You can also tell the Financial Ombudsman Service to have another look.

Yes, if a finance broker gave wrong or confusing information or advice, they might get in trouble.

Yes, there are legal experts and companies that can help you if your car finance was not sold to you the right way.

Get all the papers, messages, and notes about calls where you talked about money rules.

If the money plan was not right for you and you missed payments, it might have hurt your credit score.

Look for information about interest rates, costs, extra money you pay if you finish paying early, and see if it matches what you were told when you bought it.

The time it takes can be different. Usually, complaints take a few months to handle. It depends on how complicated the complaint is and how quickly everyone responds.

The FCA makes sure companies follow rules about money. They help keep you safe from businesses that might sell you the wrong things.

Knowing the words means you know what money you need to pay. It helps you not get into bad deals.

Looking things up online can be helpful. But it is a good idea to ask a professional for more help.

Sometimes people who sell car finance do not follow the rules. This means they might not be clear about the details when they sell it to you. This can happen with any car finance product. It's important to ask questions and understand what you are buying. You can also use a tool like a checklist to help you. This can help make sure you get the right information.

You can try to fix the problem by talking to the dealer first before getting other people or the law involved.

Ergsy Search Results

This website offers general information and is not a substitute for professional advice.

Always seek guidance from qualified professionals.

If you have any medical concerns or need urgent help, contact a healthcare professional or emergency services immediately.

Some of this content was generated with AI assistance. We've done our best to keep it accurate, helpful, and human-friendly.

- Ergsy carefully checks the information in the videos we provide here.

- Videos shown by Youtube after a video has completed, have NOT been reviewed by ERGSY.

- To view, click the arrow in centre of video.

- Most of the videos you find here will have subtitles and/or closed captions available.

- You may need to turn these on, and choose your preferred language.

- Go to the video you'd like to watch.

- If closed captions (CC) are available, settings will be visible on the bottom right of the video player.

- To turn on Captions, click settings.

- To turn off Captions, click settings again.